All Categories

Featured

Table of Contents

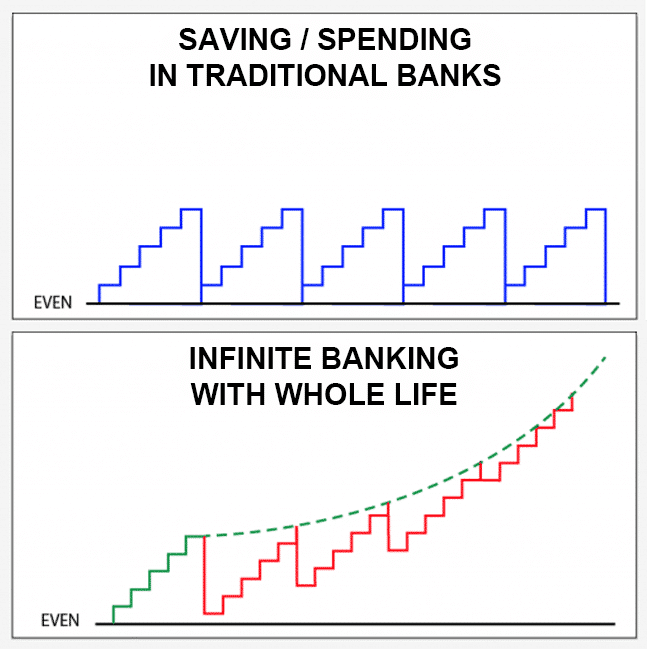

For the majority of people, the largest trouble with the infinite financial concept is that initial hit to early liquidity triggered by the costs. This disadvantage of infinite banking can be minimized substantially with correct policy layout, the very first years will certainly constantly be the worst years with any type of Whole Life plan.

That claimed, there are specific boundless financial life insurance plans created primarily for high very early money value (HECV) of over 90% in the very first year. The long-lasting performance will typically considerably delay the best-performing Infinite Financial life insurance policies. Having access to that added 4 figures in the initial few years might come at the expense of 6-figures down the roadway.

You really obtain some significant long-lasting benefits that assist you recover these very early prices and after that some. We discover that this prevented very early liquidity trouble with infinite financial is extra psychological than anything else as soon as completely checked out. In truth, if they definitely required every cent of the cash missing from their unlimited banking life insurance plan in the first few years.

Tag: infinite banking principle In this episode, I speak concerning financial resources with Mary Jo Irmen who teaches the Infinite Banking Idea. With the rise of TikTok as an information-sharing platform, financial advice and techniques have found an unique means of spreading. One such method that has actually been making the rounds is the boundless banking concept, or IBC for brief, garnering endorsements from celebs like rap artist Waka Flocka Fire.

Within these plans, the money value grows based on a rate established by the insurance company. Once a considerable cash worth gathers, insurance policy holders can acquire a cash money worth lending. These fundings differ from traditional ones, with life insurance policy functioning as security, meaning one can shed their coverage if loaning excessively without sufficient cash worth to sustain the insurance coverage expenses.

And while the allure of these policies is obvious, there are innate restrictions and dangers, necessitating thorough money worth surveillance. The strategy's legitimacy isn't black and white. For high-net-worth people or local business owner, particularly those using methods like company-owned life insurance policy (COLI), the benefits of tax breaks and compound development can be appealing.

Benefits Of Infinite Banking

The attraction of limitless banking doesn't negate its obstacles: Cost: The foundational demand, a long-term life insurance coverage policy, is pricier than its term counterparts. Qualification: Not everyone gets entire life insurance policy because of strenuous underwriting processes that can leave out those with certain wellness or way of living problems. Complexity and risk: The complex nature of IBC, paired with its risks, might deter several, specifically when less complex and much less dangerous choices are available.

Allocating around 10% of your monthly income to the policy is just not feasible for the majority of people. Component of what you check out below is merely a reiteration of what has already been said above.

So prior to you get yourself into a circumstance you're not prepared for, understand the adhering to initially: Although the principle is commonly marketed thus, you're not actually taking a finance from on your own. If that held true, you would not need to repay it. Rather, you're borrowing from the insurer and need to repay it with passion.

Some social media posts recommend making use of money value from entire life insurance coverage to pay down credit report card financial obligation. When you pay back the funding, a portion of that passion goes to the insurance firm.

For the first numerous years, you'll be paying off the payment. This makes it exceptionally challenging for your policy to gather worth throughout this time. Unless you can afford to pay a few to several hundred dollars for the following decade or even more, IBC won't function for you.

Infinite Banking Real Estate

If you call for life insurance coverage, right here are some useful suggestions to think about: Think about term life insurance. Make certain to go shopping around for the finest rate.

Copyright (c) 2023, Intercom, Inc. () with Scheduled Font Style Name "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Booked Font Style Call "Montserrat".

Td Bank Visa Infinite

As a CPA concentrating on property investing, I have actually brushed shoulders with the "Infinite Financial Concept" (IBC) more times than I can count. I've also interviewed professionals on the topic. The primary draw, besides the noticeable life insurance policy advantages, was constantly the concept of developing up cash worth within an irreversible life insurance coverage plan and loaning versus it.

Sure, that makes good sense. Truthfully, I always believed that cash would be better invested directly on financial investments instead than channeling it via a life insurance policy Till I discovered how IBC might be combined with an Irrevocable Life Insurance Coverage Depend On (ILIT) to produce generational wealth. Allow's start with the basics.

Royal Bank Infinite Visa Rewards

When you obtain against your plan's cash money worth, there's no set settlement routine, providing you the liberty to handle the financing on your terms. The cash money worth proceeds to grow based on the policy's assurances and rewards. This setup permits you to gain access to liquidity without disrupting the long-lasting growth of your policy, gave that the financing and rate of interest are handled wisely.

The process continues with future generations. As grandchildren are birthed and mature, the ILIT can purchase life insurance policy plans on their lives also. The count on then gathers several plans, each with growing money values and death benefits. With these policies in place, the ILIT efficiently becomes a "Family Bank." Household members can take financings from the ILIT, making use of the cash money worth of the policies to money investments, begin services, or cover significant expenses.

An essential element of handling this Family members Financial institution is the use of the HEMS criterion, which means "Wellness, Education And Learning, Upkeep, or Assistance." This guideline is typically consisted of in count on agreements to guide the trustee on how they can disperse funds to beneficiaries. By sticking to the HEMS requirement, the count on guarantees that distributions are made for crucial needs and lasting support, guarding the depend on's possessions while still providing for member of the family.

Enhanced Versatility: Unlike inflexible bank car loans, you manage the settlement terms when borrowing from your very own plan. This permits you to framework payments in a manner that aligns with your business capital. wealth nation infinite banking. Enhanced Money Flow: By financing business expenses via plan loans, you can possibly liberate cash that would otherwise be linked up in conventional loan settlements or equipment leases

He has the exact same devices, however has additionally built extra money worth in his plan and obtained tax obligation benefits. And also, he currently has $50,000 offered in his policy to use for future chances or expenditures., it's essential to watch it as even more than simply life insurance policy.

Is Infinite Banking A Scam

It has to do with producing an adaptable funding system that offers you control and provides several advantages. When used tactically, it can match other investments and organization methods. If you're captivated by the possibility of the Infinite Banking Idea for your service, right here are some steps to consider: Educate Yourself: Dive much deeper right into the principle with trustworthy books, seminars, or examinations with well-informed specialists.

{kind=link}

Latest Posts

Infinite Financial Systems

Benefits Of Infinite Banking

What Is A Cash Flow Banking System